Rental Bond Loans

Fast and simple loan to make rental bonds and moving expenses simple.

With 17% of Aussies having a personal loan and 13.5 million credit card accounts, there is a continuous increase in Australians applying for credit in different ways. This means that over half the Australian population has debts they need to keep track of every day.

So, what happens to your credit report if you struggle to keep up with these debts and their repayments?

On this page:

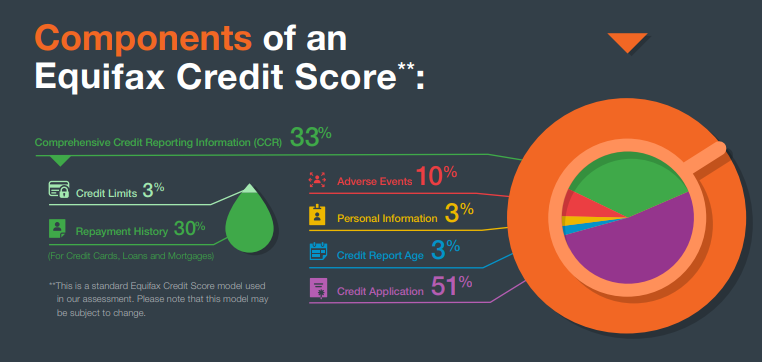

There are three main bureaus that deal with credit scores and credit reporting, Equifax, Experian, and illion, which all have a different formula to calculate people’s credit scores.

Even though each company uses a different scoring system, each uses roughly the same core information:

And more.

Did you know that for Equifax, 30% of your credit score is made up of your repayment history? This means that almost a third of your credit is from how you manage your debts.

These effects on your credit score can also impact your credit reports. Issues with these things, like late payments, can stay on your record for quite some time, especially if they’re shown as continued behaviour.

A late payment is any overdue repayment on a line of credit, such as a credit card, personal loan, mortgage, etc. If the payment is more than 14 days overdue, the banks will record it and list it as a ‘missed payment’.

However, if you make a payment over $150 more than 60 days late, it’ll be filed as a ’default’, which will stay on your credit report for a longer period of time. This doesn’t mean that you have an extra 14-day grace period from when things are due. It’s still super important to your credit score to pay on time!

A third of your credit score is made up of late payments, and if you’re not keeping up with them, it can cause major issues.

According to Experian, missing just one repayment could drop your credit score by 22%, even if it’s just a one-off fluke. This increases to 26% for two and a whopping 42% for three or more missed payments!

Continuously making late payments on credit cards or loans could massively impact your ability to get more credit in the future, as it could tell banks and lenders that you are an unreliable consumer and lead to rejected applications, which further decreases your score.

According to Equifax, if you make a payment on a credit card or loan more than 14 days late, it will be recorded on your credit report as part of your payment history. If it is a one-off mistake, followed by rectified behaviour, this is unlikely to make a prominent impact on your creditworthiness.

This information is stored in your credit report for 24 months after the initial late payment is made as long as you continue to make the rest of your repayments on time. If you default on a loan, however, this can stay on your credit report for five years. So, it’s imperative you keep track of your repayments to avoid it hurting your credit.

There are many different ways to organise your finances in order to keep track of your incomings and outgoings. Some people create spreadsheets to track their bills and budget their income accordingly. Others prefer using specially designed apps that help them track a bit more visually.

It’s important to know what fixed and debt-related expenses come out of your bank account regularly, as this gives you a better idea of what you have left to spend on things you want vs. need. Setting up direct debits or setting yourself reminders can really help, as can budgeting apps. It’s also a good idea to consider asking your lender if your repayments can be made on the same day you get paid.

If you’re struggling with money or debts, you can call the free National Debt Helpline on 1800 007 007 (Monday – Friday). Aboriginal and Torres Strait Islander peoples can also contact the free Mob Strong Debt Helpline on 1800 808 488.

ASIC MoneySmart also recommends doing the following:

If managing multiple debts becomes overwhelming, you could consider a debt consolidation loan. This option merges debts into one manageable payment, simplifying tracking your due dates if that’s the main cause of the issues.

Our debt consolidation loans let you borrow between $3,000 and $25,000 over 25 months - 36 months. They’re also a highly flexible product and can be used for a number of common debts.