Rental Bond Loans

Fast and simple loan to make rental bonds and moving expenses simple.

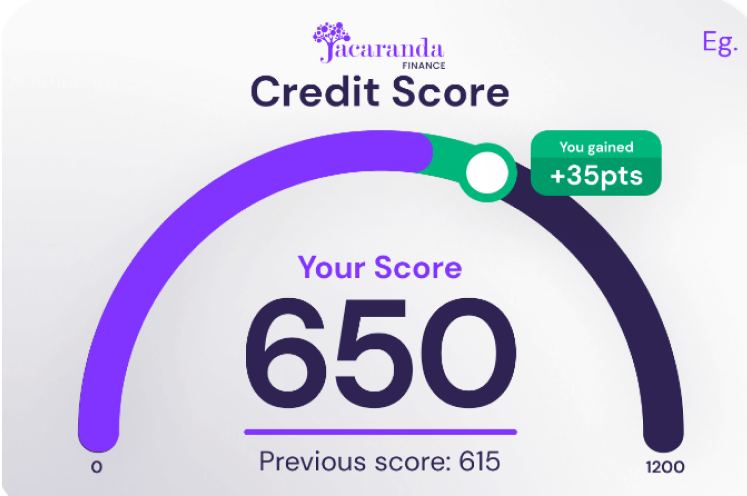

Get rewarded for positive credit repayments

Learn how Comprehensive Credit Reporting (CCR) could help you improve your credit score and enhance your financial opportunities.

Every year, the banks fail millions of Aussies who need to borrow money. This is often purely because they don't have a high credit score, even if they've been good with money lately.

We think that's unfair, as your credit score doesn't define you. So, when that happens to you, come and talk to us.

We're an Australian-owned, operated, fully online digital lender providing fast and flexible loans.

Click here to learn more about what makes Jacaranda Finance great!

Comprehensive Credit Reporting (CCR for short) refers to sharing more comprehensive customer information between credit providers and credit reporting bodies. Sometimes known as Positive Credit Reporting, it means someone's positive credit behaviour can now be seen on their credit report, such as:

And more. Previously, credit reports only flagged negative credit behaviours, such as missed repayments, hard credit inquiries, payment defaults, infringements, and more. This was sometimes called 'Negative' Credit Reporting and wasn't as thorough.

Positive information being available to credit providers can result in more accurate assessments of your suitability for finance products and give them more insight into your creditworthiness, as they'll have a better picture of your repayment history and ability to manage your finances.

Jacaranda Finance is reporting data under the Comprehensive Credit Reporting regime.

With CCR, we will now provide a more detailed and comprehensive view of your credit history to credit bureaus.

This means that your credit behaviour, such as making timely repayments and managing your loans responsibly, will be reported, which could potentially strengthen your credit profile.

You may also have improved access to more competitive loan products, better loan terms and increased transparency in your credit information.

CCR could help you in a number of ways, which we’ve summarised below.

For a more detailed overview of both the pros and cons of CCR, see our article here.

CCR allows credit providers to access a more complete picture of an individual's credit history to make more informed decisions about lending to consumers.

If you have a strong recent credit history, CCR could make you eligible for more competitive products.

People who've positively changed their credit behaviour may see their credit score improve faster under CCR than under negative credit reporting.

Things like defaults or bankruptcies can stay on your credit report for years. So, if you fell on hard times just once but have demonstrated good credit behaviours, CCR can highlight this to credit providers.

While a credit report provides a snapshot of your financial track record, comprehensive credit reporting offers a more complete picture. With comprehensive credit reporting (CCR), lenders can see more than just past mistakes. Your credit report could also include positive information, like whether you make repayments on time and how much credit you’re using. It’s another way that we can assess how you’re managing money today – not just your past. Read more: What is Comprehensive Credit Reporting?

If a traditional credit report is your score on the final exam, comprehensive credit reporting is your study habits, classes attended and grades. This means that a mistake in your past doesn’t have to define your future. Instead, with CCR lenders can see the big picture. It also means that with good financial habits, your credit score could improve.

Unlike a traditional credit report which only includes any mistakes you’ve made, comprehensive credit reporting records both positive and negative credit behaviours. This could include whether you make repayments on time and any financial hardship variations you enter.

Read more: What is Comprehensive Credit Reporting?

Repayment history information is generally shown for up to 24 months. This includes whether repayments were made on time or late during that period. Note that if you miss a repayment, make a late payment or default on your loan, this may appear separately on your credit report.

Checking your credit report can help you to better understand your credit position. You can access your credit report for free every 3 months (or more frequently however costs may apply) through a credit reporting agency such as Equifax or Experian, or a third-party service such as ClearScore. In order to access your credit report, you may be required to verify your identity.

A credit score (also known as a credit rating) is a 1-4 digit number that reflects your credit worthiness and how reliable you are when borrowing money and repaying it. Higher scores indicate a positive credit history while lower scores signal more risk to lenders. Read more: Credit scores explained

When you apply for a loan, lenders use your credit score to help them assess your application. This includes: A lower credit score could make it more difficult to be approved for new credit and is often associated with higher interest rates. A higher credit score could improve your chances of a successful loan application and potentially give you access to better rates and more flexible terms. Read more: How to improve your credit score?

Credit scores are calculated using information from your credit report, including: Read more: How to improve your credit score?