Rental Bond Loans

Fast and simple loan to make rental bonds and moving expenses simple.

Apply in minutes1 and get a same day outcome2

Subject to lending criteria, terms and conditions. See below for details.

Subject to lending criteria, terms and conditions. See below for details.

Award-winning lender

We know when unexpected costs come your way you don’t have time to wait. While banks can take up to a week (or just say no), we use a smarter, faster way to assess your situation.

Our award-winning system looks beyond your credit score, using your real bank statement data to find a path to yes – even if your bank won't.

And when it comes to your privacy, we take it seriously. We use bank-level security and 256-bit encryption to keep your data safe.

Broken down car? Had to rush your pet to the vet? If you’ve been hit with an unexpected expense, don’t worry. Jac’s got your back. Apply online and get a fast outcome when you need it most.

Learn more about our personal loans

Been rejected by the bank? We look beyond your credit score to see your real financial situation. Our flexible approach means you could still be approved – even when others say no.

Get a fair shot at funding

With Comprehensive Credit Reporting (CCR), your on-time repayments can positively impact your credit score. Potentially making it easier to access better rates in the future.

We believe in second chances

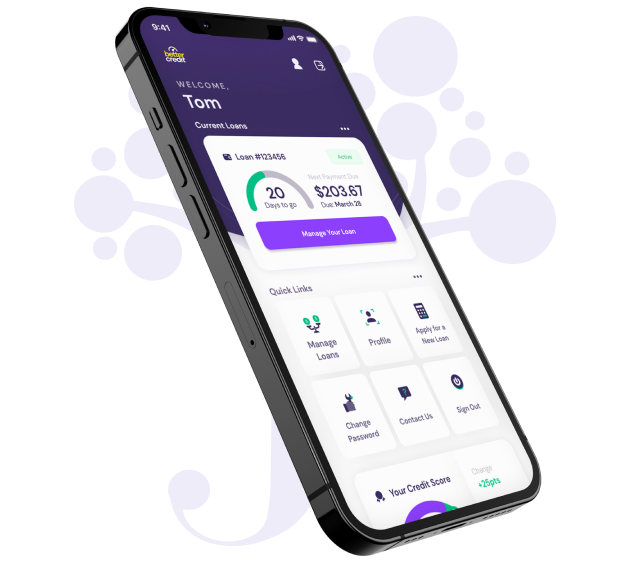

Manage your Jacaranda Finance loan in one easy, secure app - anytime, anywhere.

Apply by 3:00pm with everything we need, and you’ll get your loan outcome that same day2 — simple as that.

No waiting, no wondering. Just clarity and speed when you want to get behind the wheel fast. Most banks take days to respond. Thanks to our clever tech, we move in hours because your time matters.

We know you’re more than a credit score and sometimes life doesn’t fit inside a bank’s checklist.

That’s why we take a different approach. By securely reviewing your recent bank statements, we build a clearer picture of your financial situation — one that gives you a real shot at approval.

It’s a fairer way to assess, and a faster way to move forward.

One second, everything is going great. The next, you’re being told your car needs repairs, have a holiday coming up – and oh, that home repair you’ve been putting off has gone from bad to worse.

When life hits you hard, you need a fast moving lender that looks beyond your credit score. At Jacaranda Finance, we can make personal loans happen when the banks won’t.

We’re not a bank. We’re a smarter kind of lender that looks beyond credit scores to understand your real financial health. Our clever Edge Score system uses extra data from your bank statements to see how you're managing money today - not just your past.

It’s fast, simple, and secure and it could help you get the funds you need, when you need them most. That’s what sets us apart.

Before you apply for a loan, we think it's important to review your budget and be certain that you can comfortably repay it.

Once you know what you can afford in your budget, use our loan repayment calculator to estimate your repayments before you apply.

Ready to Apply? You can get started now.Our loans are designed to be fast, fair, and, above all, affordable, with no hidden fees. See the table below for a quick guide to our charges, or visit our fees page to learn more. For detailed information about who our products are designed for, please review our Target Market Determinations.

Am I eligible for a Loan with Jacaranda Finance?

You must meet the following basic eligibility criteria before submitting an application:

A personal loan is a fixed-term loan that allows you to borrow a set amount of money and repay it through regular instalments. Our online application process is designed to be fast and straightforward. Repayments remain consistent throughout the loan term so you can plan your budget with confidence.

Applying is Quick & Easy

Ready to get started? Apply now.

By submitting a full application for a personal loan, you are authorising a hard credit check. This means that other lenders will be able to see that you applied for a loan and could impact your credit score. Before you submit a full application with Jacaranda Finance, you can check if you qualify with no impact on your credit score*. This is called a soft credit check, and is only visible on your credit report to you.

How to check if you qualify for a secured personal loan?

If you’re considering applying for a loan with Jacaranda Finance, you can check if you qualify with no impact on your credit score*.

No, checking if you qualify uses a “soft” credit check meaning it does not impact your credit score or appear on your credit file to anyone but you. We recommend checking your eligibility before applying for a loan where possible to reduce the number of applications on your credit report.

To be assessed for a loan from Jacaranda Finance, you must meet the following basic eligibility criteria:

If you are unsure whether you’re eligible, you can check if you qualify with no impact on your credit score*.

We offer two main products at Jacaranda Finance:

For detailed information about who our products are designed for, please review our Target Market Determinations. Our Loan Repayment Calculator and our guide to Jacaranda Finance’s interest rates & fees could help you to predict your repayments before applying.

Using our loan repayment calculator you can estimate your repayments before applying.

Missed Payment Fees

For every missed payment, a fee will be applied. This cost is added to the account balance and can be paid with the next repayment cycle. If you’re concerned you’ll miss a repayment before the next due date, please contact our customer support team as soon as possible.

You can pay your loan back at any time at no extra cost. That means no early exit or payout fees.

Once you’ve been approved and have accepted your loan contract, we’ll automatically attempt to release the money to your account. Most customers get paid in 60 seconds3.

6,141 people have already started an application in the last 7 days.